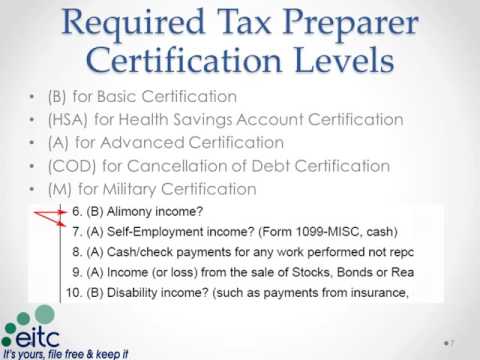

Welcome to lesson three, the intake and interview. This shows the full steps of the intake and interview process that each volunteer will go through with every single taxpayer that comes into the tax sites. The taxpayer will first fill out an intake sheet, and then the volunteer will complete an interview. You will check their identification and individual tax forms, prepare the return, and then have another volunteer do a quality review. Now, we're going to go through each of these steps one by one. When a taxpayer comes to the tax site, the very first thing that he or she will do is to fill out this intake form. This is all their basic information right here at the top: their name, their address, birthday, etc. And then below that, it would be the same for their spouse if there was one. This form will also help you determine their filing status and how many dependents they have. As you can see down here in part two, it's the marital status and household information. This is the section you will use to determine their filing status. If they are single with no dependents listed down there, then they'll most likely qualify as single. If they're single with dependents listed below, they may qualify as single or head of household. I just want to point out that we do have a lesson on filing status, dependents, and exemptions, and I encourage you to watch that training video if you have more questions about that specifically. Below the marital status section, you can see by this green arrow here, it says, "List the names below of everyone who lived with you and/or anyone you supported but did not live with you during the tax year." Sometimes, this section gets a little confusing for...

Award-winning PDF software

13614 Form: What You Should Know

IR-INF-2-01. IR-06-1361. For additional information, refer to IRS Publication 519, Employer's Tax Guide to the Foreign Earned Income Exclusion, the Instructions for Form 8621—Foreign Earned Income Credit, and the Forms and Publications section of the Publication 1603. IR-06-1361. IRS Form 8621: Foreign Earned Income Credit. IR-06-1361. The Foreign Earned Income (FIE) exclusion is available to U.S. citizens, resident aliens, and certain other individuals. The exclusion may be claimed by a taxpayer who has income from sources within or outside the U.S. or by an employer if the taxpayer has foreign earned income that is effectively connected with the conduct of a trade or business within the United States, or a U.S. foreign corporation (or other entity treated as such); However, the FIE exclusion is not available to individuals who are employees of U.S. corporations. The taxpayer must satisfy the minimum dollar amount requirement and also meet a test requirement. The minimum dollar amount is the gross income of the taxpayer (as assessed on the most recent return for that taxable year), reduced by the taxpayer's share of foreign income. The taxpayer's share of the foreign income is treated as earned income by the foreign corporation; The taxpayer's test requirement is satisfied if the test applies to the foreign income. The test is not satisfied if the foreign income is exempt income. See Section 1254(b) of the Revenue Act of 1978, as amended, for more information. Foreign income is defined as all income from sources within and outside the United States. Section 1255 of the IRS Code defines foreign income as any income from sources within the U.S. and any income from sources outside the U.S. When a taxpayer's foreign sources of income do not exceed the limitations set forth in section 1255(b), the foreign source income is considered fully taxable income, and the taxpayer uses the following definitions to determine whether the taxpayer paid the applicable income tax. Foreign source income is income from sources within, or outside, the United States. For U.S. sources of income, the foreign source income is the excess of the U.S. income over the U.S. source income.

Online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 13615, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 13615 online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 13615 by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 13615 from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Form 13614